- The Inflation Reduction Act (IRA) could be the biggest target for a second Trump administration

- Drastic repeal of IRA production tax credits is unlikely

- Current market trends already favour blue hydrogen, suggesting policy may follow industry preferences

Globally, 2024 is the year when the largest number of people ever will go to the polls for nationwide elections. With each year being crucial to the planet limiting climate change, and with the speed and spread of new energy deployment being critical to this mission, the potential impact of these elections cannot be understated.

The prominence of the locations with potential governmental change is striking, too, with nine of the G20 members holding elections. Eight out of these nine of these have had their elections already. It is the final member’s general election among these nine, the US, that commentators fear could have the largest effect on climate policy, particularly if Donald Trump were to win a second term. While polls have narrowed since Kamala Harris became the de facto Democrat party candidate, in key swing states Trump retains a lead at the time of writing.

HySights contention is that this effect would largely be felt internationally rather than within the US, though, given existing market trends.

The IRA lightning rod

A recent bi-partisan habit has been for the incoming President to ditch – in a highly public manner – a flagship policy of their predecessor. It is consequently no surprise that speculation has been on the rise on how safe elements of the IRA are were Trump to win the election.

Compared to the Infrastructure Investment and Jobs Act (IIJA) or Bipartisan Infrastructure Law (BIL), which was passed with bipartisan support and therefore less likely to be rolled back, the IRA was pushed through by Democratic lawmakers in 2022 and represents the single largest investment in new energy spending in US history.

For transition finance (areas such as hydrogen and its derivatives, some biofuels, and carbon capture), production tax credits for lower carbon hydrogen (45V) and carbon capture (45Q) will prove vital to help kick start production and projects in these nascent sectors. However, most of the IRA-influenced investment so far, according to US Treasury numbers, have been announced in solar and energy storage (69% of $336 billion according to a statement made by the Treasury in 2024), whereas just 13%, or $43 billion, has been announced for hydrogen and carbon management.

While this is no small change, how much of it has been deployed or earmarked for projects that have reached a Final Investment Decision (FID) is a greyer area. The guidelines around the 45V production tax credit have been criticised by the prospective hydrogen producers, and have yet to be finalised by the US Treasury Department. Plug Power is one of the few companies to include 45V credits in its financial statements.

Republican party ire has been focused on a few technologies that appear prominently in the IRA, such as electric vehicles. At the 2024 Republican National Convention, Trump has promised to end the “electric-vehicle mandate on day one”. Given a significant portion of planned IRA-prompted investment is focused on both energy storage and battery manufacturing, it would be fair to consider this part of the IRA at highest risk of repeal or watering down.

How a Trump administration would handle carbon capture, utilisation and storage (CCUS) technologies is less clear. While Trump has proposed cuts for the US Department of Energy’s (DOE) carbon capture and storage research, he also did sign two bipartisan acts into law that incentivised the CCUS industry: the Bipartisan Budget Act (BBA) of 2018 and the Utilising Significant Emissions with Innovative Technologies (USE IT) Act of 2020.

While Trump’s own views and those of his Republican party supporters are important to future industrial policy, the balance of power in the two houses of Congress as well as election cycles are important variables, too. Any roll back of the IRA’s production tax credits will need majorities from both congressional chambers, and many projects benefitting from the IRA are in traditionally Republican as well as competitive swing states, such as Georgia and Michigan.

Amplification of market trends

A Trump administration that favours blue new energy products over renewable or green equivalents can be viewed as a reflection of today’s preferences from market participants.

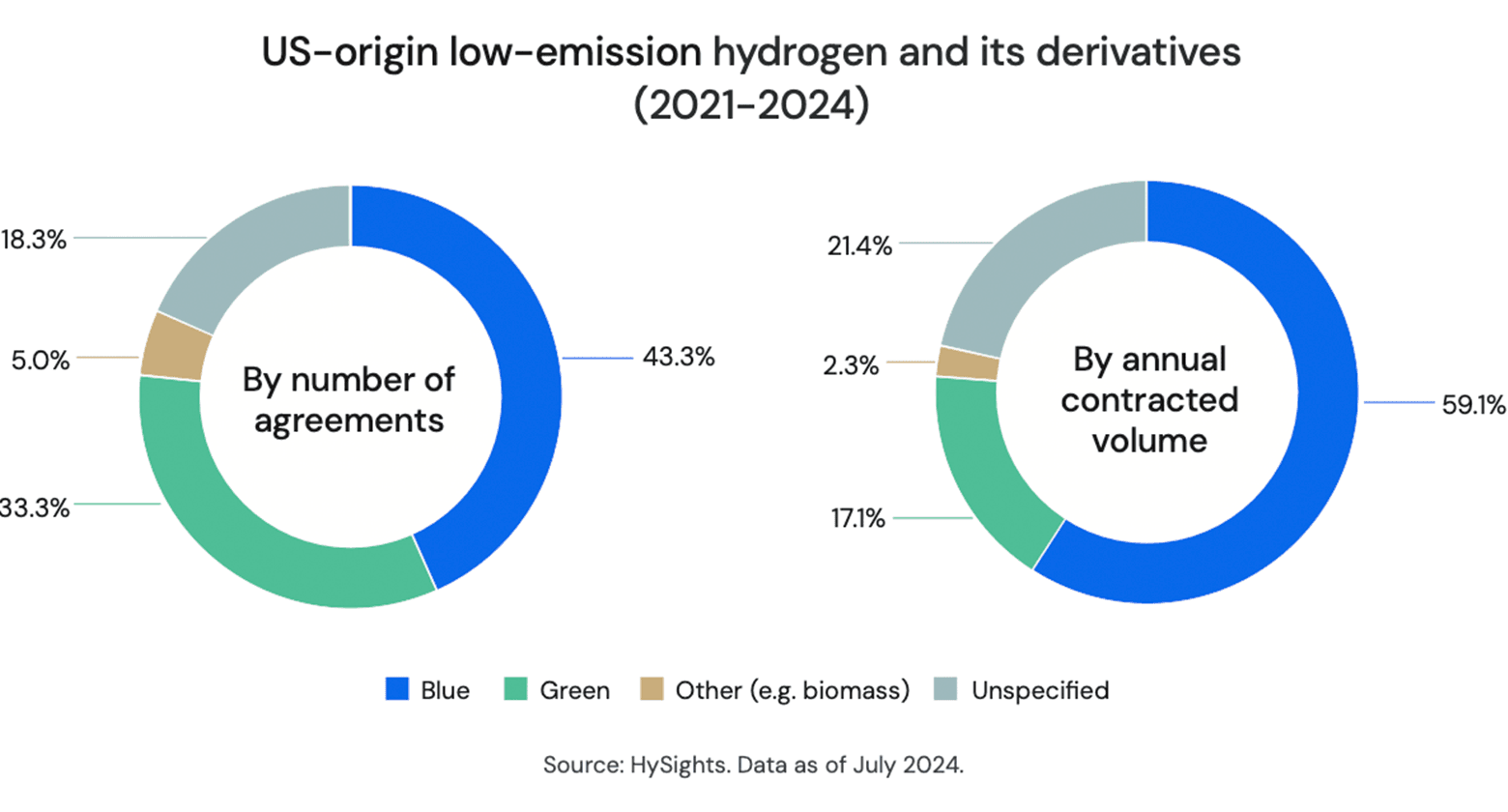

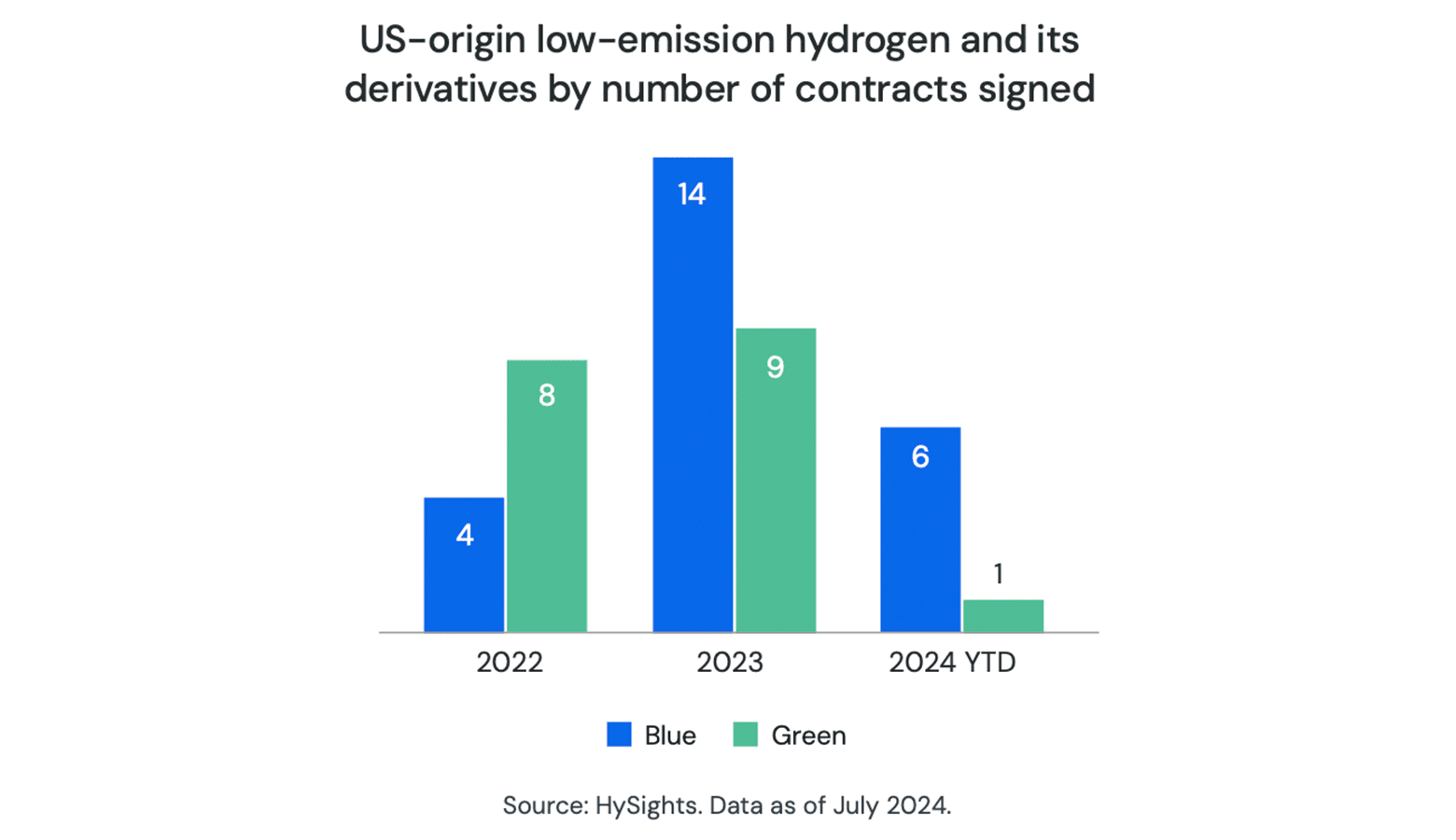

According to HySights data, while the 62 contracts announced relating to US-origin hydrogen and its derivatives are evenly split between blue and green production routes, there is a much larger portion of hydrogen-equivalent annual tonnage attributed to blue contracts: 1,007,777 metric tonnes (mt) compared to 664,507 mt from green contracts.

Industry players have also come out against radical repeals of the IRA. Most notably, chief executive of the American Petroleum Institute (API) Mike Sommers, the country’s largest oil and gas trade association and lobby group, has stated at that “a lot of great provisions in the IRA” including the 45V and 45Q credits are important to the industry, and should remain.

The green contracts tend to be associated with mobility as an end-use, and US-focused; the blue contracts are more export-oriented and with more varied end use cases.

Furthermore, in a sign of where momentum is today, there have been eight blue contracts signed for US-origin hydrogen and derivatives in 2024, versus four for green. One European new energy project developer confided with HySights that, while green hydrogen projects were publicly still being pursued, blue US hydrogen projects were their focus.

The uncertainty caused by the US election can be seen in an overall reduction in the number of contracts signed in 2024 for US-origin low-emission fuels. This has allowed other countries, especially India, which has a highly visibly supportive administration to these fuels, to steal ahead. India-origin contracts account for 20% of all contracts signed in 2024, versus just 6.5% in 2023.

For low-carbon hydrogen, there would consequently be more continuity in terms of industry’s direction were Trump to win the next election than many commentators currently seem to think, with CCUS-related blue projects possibly being more favoured from a policy perspective as well as an industry perspective, were Trump to win.

In fact, there have been few radical policy changes around the world this year when it comes to transition finance commodities. Whether elections have resulted in increased vote share from parties on the edges of the political spectrum (EU, France), or major change in parliamentary balance of power (UK), the changes have more been ones of emphasis rather than material. The EU’s inclusion of blue hydrogen in its legal definition of “low-carbon hydrogen” may be one such example.

The focus of both the previous Trump and the Biden administration to “reshore” manufacturing and enable production of new energy technologies in the US is likely to appeal to whomever is next occupying the White House. In that sense, the industrial policies of both administrations differs less than their foreign policy outlook, and their stance towards multilateral institutions.

It is in this sphere that new energy may be most under threat, given the Trump-led US withdrawl from the Paris Agreement on Climate Change in 2020, while comments about the effectiveness of the UN and also of NATO may have implications for geopolitical stability more broadly than solely in energy markets. While the direct impact of multilateral institutions on national climate policy can be disputed, an environment of international collaboration via these institutions is generally seen as crucial to positive, and swift action on combatting climate change.

Learn more about HySights Ratings

To request a demo or HySights Ratings methodology, reach us at contact@hysights.com

Access market insights