Geologic hydrogen – naturally occurring molecular hydrogen found in underground deposits – has enjoyed renewed interest over the past year, representing a previously untapped energy source with a potential cost and emissions intensity (EI) lower than that of manufactured hydrogen via renewable energy or even fossil fuels.

Also known as natural, gold, or white hydrogen, this resource results from serpentinisation (iron-rich mineral reactions with water), radiolysis (radioactive decay splitting water molecules), or other deep-earth processes. Extraction approaches range from direct recovery at natural seeps to stimulated production using chemical or thermal enhancement techniques.

Since 2024, investment momentum has accelerated, with major players including Bill Gates’ Breakthrough Energy Ventures, Mitsubishi Heavy Industries, BP Ventures, Rio Tinto, and Fortescue committing resources to exploratory efforts.

Transformative cost potential

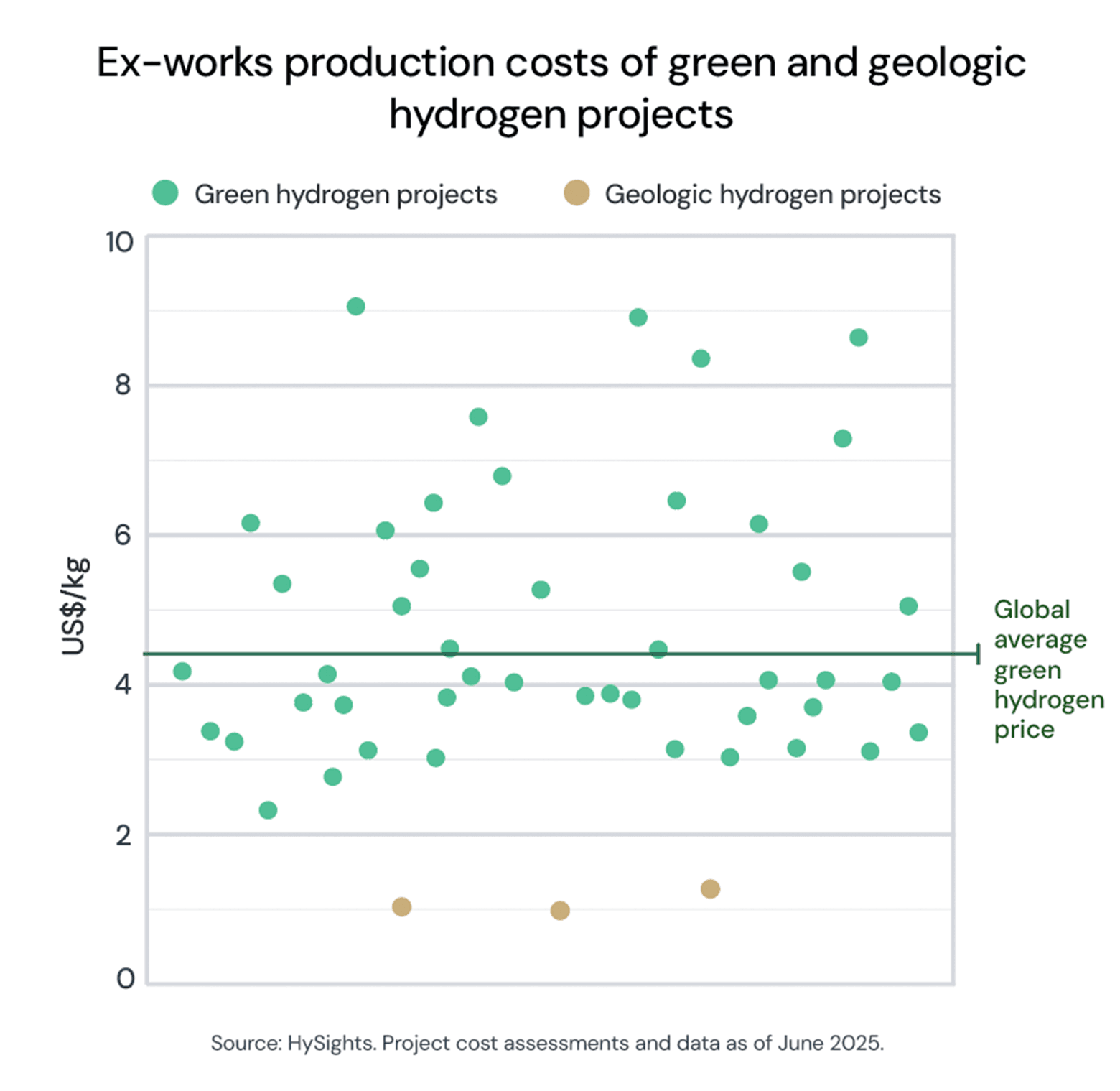

Recent techno-economic analyses point to geologic hydrogen’s transformative cost potential. A January 2024 Stanford study estimates production costs of $0.54/kg for natural and $0.92/kg for stimulated geologic hydrogen under optimal US conditions. These figures align with natural hydrogen exploration company Mantle8’s modelling from their Comminges prospect in the French Pyrenees, which indicates €0.8/kg ($0.94/kg) at the wellhead.

The EFI Foundation’s June 2025 report corroborates these ranges, citing industry estimates of $0.40–$1.50/kg for geological hydrogen, with potential for further cost reductions as technologies mature.

At these numbers, geological hydrogen not only represents an extraordinary cost advantage over today’s green hydrogen – at an average of $4.32/kg globally and $5.65/kg in Europe – under some scenarios it matches or beats grey hydrogen from steam methane reforming (SMR), which currently dominates global supply at less than $2/kg average cost.

This positions geologic hydrogen as the first potential low-emission hydrogen source that could compete economically with fossil fuel-derived hydrogen without a runway of government subsidies.

Robust environmental credentials

Geologic hydrogen’s low-carbon profile emerges from its natural production mechanism. Its primary emissions sources remain embodied carbon from drilling operations and potential fugitive emissions – both manageable through diligent operators and oil and gas industry best practices.

A 2023 Stanford Life Cycle Assessment (LCA) published in Joule calculated geologic hydrogen carbon intensity (CI) at 0.37 kgCO2e/kgH2 for a “generic” production site including the embodied emissions of the well casing and hydrogen emissions. Notably, this value assumes a gas mix of 85% hydrogen and 1.5% methane. At 75% hydrogen and 22% methane, the intensity rises to 1.5 kgCO2e/kgH2.

This represents the lowest carbon intensity among all hydrogen production pathways, surpassing even renewable-powered electrolysis when accounting for embodied emissions.

Additionally, these levels of EI (e.g. below 2 kgCO2e/kgH2) are likely to meet nearly all national definitions of low-emission hydrogen globally, allowing geologic hydrogen projects to meet necessary regulatory requirements.

Economic realities and cost drivers

Despite enthusiasm, substantial uncertainties persist. Resource quality and site location remain critical variables determining geologic hydrogen project bankability and cost.

Hydrogen purity and gas composition: The Mali well site – the posterchild for geologic hydrogen production – hydrogen purity of 98% represents the ideal scenario. Most prospects report 70%–90% hydrogen, such as Gold Hydrogen’s South Australian Ramsay 2 showing high 86% concentrations. The relationship between purity and processing costs creates step-change economics at certain thresholds. The costs of gas separation can severely impact geologic hydrogen and bring the cost above the average cost of green hydrogen on an ex-works basis.

Flow dynamics shape viability: Unlike manufactured hydrogen’s predictable output, geologic production depends on reservoir characteristics. High-flow wells are able to amortise drilling and infrastructure fixed costs across larger volumes.

These fixed costs are not insignificant: European exploration drilling typically requires €10-15 million ($11.5-17.3 million) per well, based on recent French operations. In the US, drilling costs average $4 million for natural hydrogen wells and $6.7 million for stimulated production.

To give a base case view, the 2024 Stanford techno-economic analysis calculates these thresholds of achieving sub-$1/kg geologic hydrogen:

-

For natural deposits: Minimum 75 kg H2/hr flow rates and hydrogen purity level above 50%

-

For stimulated production: Minimum 175 kg H2/hr flow rates and purity levels exceeding 65% due to its additional processing costs

Distance to markets and transportation: Distance to consumption centres remains a crucial economic factor with geologic hydrogen as with manufactured hydrogen – an area often underestimated in early-stage project evaluation. Pipeline transport still offers the most economical solution, and projects near industrial clusters or existing demand centres would enjoy clear economic advantages.

Land use and regulatory complexity: Land acquisition and mineral rights vary dramatically by jurisdiction, from streamlined processes in jurisdictions like South Australia (which added hydrogen to regulated substances in 2021) to complex negotiations in regions with unclear subsurface ownership frameworks.

Scale limitations: Most planned geologic hydrogen sites are expected to reach 5,000–15,000 tonnes per annum production capacity, which positions it as a complementary rather than dominant supply source.

And while most individual geologic hydrogen sites do not match the scale of mega-projects planned for green or blue hydrogen (regularly targeting 100,000+ tonnes/year), their potential superior economics position may serve the need for specific industrial applications in a region. Market outlook

Current exploration momentum suggests 2025-2027 will prove pivotal for sector viability, with first production results providing crucial data on flow rates, gas compositions, and project economics.

Based on current data, is unlikely that geologic will displace large-scale green or blue hydrogen production but it will occupy an important niche in the emerging hydrogen economy. Its role parallels that of distributed solar in the electricity sector – providing localised, cost-effective supply that complements rather than competes with utility-scale generation.

Learn more about HySights Ratings

To request a demo or HySights Ratings methodology, reach us at contact@hysights.com

Access market insights